Biological Assets

[Submitted by CA. Divya Balasubramanian,

Chartered Accountant]

October 12, 2011

When I first heard this word my head went for a tizzy. I started thinking of all possible explanations, could it mean surgical equipments to something vaguely related to biology but then I did the obvious, yes googled it and voila IAS-41 came to my rescue.

This article intends to provide a crisp and brief understanding of the term “Biological Assets” in Accounting and IAS-41.

What does it mean?

Biological assets are living plants or animals, such as trees in a plantation or orchard, cultivated plants, sheep and cattle, etc. The term was introduced in International Accounting Standard 41, Agriculture.

It applies to biological assets, agricultural produce at the point of harvest, and government grants related to biological assets.

The table below provides examples of biological assets, agricultural produce, and products that are the result of processing after harvest:

| Biological assets | Agricultural produce | Products that are the result of processing after harvest |

| Trees in a plantation forest | Felled trees | Logs, lumber |

| Plants | Cotton | Thread, clothing |

| Harvested cane |

Sugar |

|

| Pigs | Carcass | Sausages, cured hams |

| Bushes | Leaf | Tea, cured tobacco |

| Vines | Grapes | Wine |

| Fruit trees | Picked fruit | Processed fruit |

As per above table agriculture produce would be considered as a biological asset only up to the point of harvest

How should an entity recognize it

An entity should recognize a biological asset or agriculture produce only when the entity controls the asset as a result of past events, it is probable that future economic benefits will flow to the entity, and the fair value or cost of the asset can be measured reliably.

Examples

Sheep and Lamb are Biological Assets however the wool sheared from the sheep is an Agricultural Asset.

How should an entity Measure its Biological Assets

Briefly stating the parameters in IAS 41 below:

-

Biological assets should be measured on initial recognition and at subsequent reporting dates at fair value less estimated costs to sell, unless fair value cannot be reliably measured. [IAS 41.12]

-

Agricultural produce should be measured at fair value less estimated costs to sell at the point of harvest. [IAS 41.13] Because harvested produce is a marketable commodity, there is no 'measurement reliability' exception for produce.

-

The gain on initial recognition of biological assets at fair value less costs to sell, and changes in fair value less costs to sell of biological assets during a period, are reported in net profit or loss. [IAS 41.26]

Impact on Reporting as per Indian Accounting Standards (IGAAP)

Under IGAAP, AS 10 and AS 2 have scoped out the treatment for biological assets. Hence, there is no guidance available under IGAAP for the accounting of biological assets.

However if an organization wants to follow IAS 41, for better reporting and transparency, it shall have to disclose that the treatment is done as per IAS 41 and not, as per IGAAP.

Other standards applicable to Biological Assets

IAS 20, Accounting for Government Grants and Disclosure of Government Assistance ;

IAS 36, Impairment of Assets, when biological assets are measured at fair value.

Now that a little light has been shone on Biological assets, the next time, you see an animal remember It’s a Biological Asset

Tax Haven - What is it?

[Submitted by CA. Vibhuti Gupta,

Chartered Accountant,

New Delhi]

August 31, 2010

TAX HAVEN : A tax haven is a country or territory where certain taxes are levied at a low rate or not at all.

In its December 2008 report on the use of tax havens by American corporations, the U.S. Government Accountability Office regarded the following characteristics as indicative of a tax haven:

- nil or nominal taxes;

- lack of effective exchange of tax information with foreign tax authorities;

- lack of transparency in the operation of legislative, legal or administrative provisions;

- no requirement for a substantive local presence; and

- self-promotion as an offshore financial center.

Advantages of tax havens are viewed in four principal contexts :-

- Personal residency. Since the early 20th century, wealthy individuals from high-tax jurisdictions have sought to relocate themselves in low-tax jurisdictions. In most countries in the world, residence is the primary basis of taxation. In some cases the low-tax jurisdictions levy no, or only very low, income tax. But almost no tax haven assesses any kind of capital gains tax, or inheritance tax.

- Asset holding. Asset holding involves utilizing a trust or a company, or a trust owning a company. The company or trust will be formed in one tax haven, and will usually be administered and resident in another. The function is to hold assets, which may consist of a portfolio of investments under management, trading companies or groups, physical assets such as real estate. The essence of such arrangements is that by changing the ownership of the assets into an entity which is not resident in the high-tax jurisdiction, they cease to be taxable in that jurisdiction. Often the mechanism is employed to avoid a specific tax. For example, a wealthy testator could transfer his house into an offshore company; he can then settle the shares of the company on trust (with himself being a trustee with another trustee, whilst holding the beneficial life estate) for himself for life, and then to his daughter. On his death, the shares will automatically vest in the daughter, who thereby acquires the house, without the house having to go through probate and being assessed with inheritance tax. (Most countries assess inheritance tax (and all other taxes) on real estate within their jurisdiction, regardless of the nationality of the owner, so this would not work with a house in most countries. It is more likely to be done with intangible assets.)

- Trading and other business activity. Many businesses which do not require a specific geographical location or extensive labor are set up in tax havens, to minimize tax exposure, for examples include internet based services and group finance companies. In the 1970s and 1980s corporate groups were known to form offshore entities for the purposes of "re-invoicing". These re-invoicing companies simply made a margin without performing any economic function, but as the margin arose in a tax free jurisdiction, it allowed the group to "skim" profits from the high-tax jurisdiction. Most sophisticated tax codes now prevent transfer pricing scams of this nature.

- Financial intermediaries. Much of the economic activity in tax havens today consists of professional financial services such as mutual funds, banking, life insurance and pensions. Generally the funds are deposited with the intermediary in the low-tax jurisdiction, and the intermediary then on-lends or invests the money (often back into a high-tax jurisdiction). Although such systems do not normally avoid tax in the principal customer's jurisdiction, it enables financial service providers to provide multi-jurisdictional products without adding an additional layer of taxation. This has proved particularly successful in the area of offshore funds.

The OECD and tax havens -

The Organisation for Economic Co-operation and Development (OECD) identifies three key factors in considering whether a jurisdiction is a tax haven:

- Nil or only nominal taxes : Tax havens impose nil or only nominal taxes (generally or in special circumstances) and offer themselves, or are perceived to offer themselves, as a place to be used by non-residents to escape high taxes in their country of residence.

- Protection of personal financial information: Tax havens typically have laws or administrative practices under which businesses and individuals can benefit from strict rules and other protections against scrutiny by foreign tax authorities. This prevents the transmittance of information about taxpayers who are benefiting from the low tax jurisdiction.

- Lack of transparency: A lack of transparency in the operation of the legislative, legal or administrative provisions is another factor used to identify tax havens.

Anti-avoidance

To avoid tax competition, many high tax jurisdictions have enacted legislation to counter the tax sheltering potential of tax havens. Generally, such legislation tends to operate in one of five ways:

- Attributing the income and gains of the company or trust in the tax haven to a taxpayer in the high-tax jurisdiction on an arising basis. Controlled Foreign Corporation legislation is an example of this.

- Transfer pricing rules, standardization of which has been greatly helped by the promulgation of OECD guidelines.

- Restrictions on deductibility, or imposition of a withholding tax when payments are made to offshore recipients.

- Taxation of receipts from the entity in the tax haven, sometimes enhanced by notional interest to reflect the element of deferred payment. The EU withholding tax is probably the best example of this.

- Exit charges, or taxing of unrealized capital gains when an individual, trust or company emigrates.

Incentives

There are several reasons for a nation to become a tax haven. Some nations may find they do not need to charge as much as some industrialized countries in order for them to be earning sufficient income for their annual budgets. Some may offer a lower tax rate to larger corporations, in exchange for the companies locating a division of their parent company in the host country and employing some of the local population. Other domiciles find this is a way to encourage conglomerates from industrialized nations to transfer needed skills to the local population.

Examples

|

|

Former tax havens

- Beirut formerly had a reputation as the only tax haven in the Middle East. However, this changed after the Intra Bank crash of 1966 and the subsequent political and military deterioration of Lebanon dissuaded foreign use as a tax haven.

- Liberia had a prosperous ship registration industry. The series of violent and bloody civil wars in the 1990s and early 2000s severely damaged confidence in the jurisdiction. The fact that the ship registration business still continues is partly a testament to its early success, and partly a testament to moving the national Shipping Registry to New York City.

- Tangier had a brief but colorful existence as a tax haven in the period between the end of effective control by the Spanish in 1945 until it was formally reunited with Morocco in 1956.

- A number of Pacific based tax havens have ceased to operate as tax havens in response to OECD demands for better regulation and transparency in the late 1990s.

Lost tax revenue

Estimates by the OECD suggest that by 2007 capital held offshore amounts to somewhere between US$5 trillion and US$7 trillion, making up approximately 6–8% of total global investments under management. Of this, approximately US$1.4 trillion is estimate to be held in the Cayman Islands alone.

In October 2009 research commissioned from Deloitte for the Foot Review of British Offshore Financial Centres indicated that much less tax had been lost to tax havens than previously had been thought. The report indicated "We estimate the total UK corporation tax potentially lost to avoidance activities to be up to £2 billion per annum, although it could be much lower." The report also dissected an earlier report by the TUC, which had concluded that tax avoidance by the 50 largest companies in the FTSE 100 was depriving the UK Treasury of approximately £11.8 billion. The TUC's analysis had looked at the reported profits of the companies and the amount of tax paid, which created a gap in tax revenues which was mostly due to differences in the accounting treatment of profit for taxation purposes, which were intended under the UK's tax rules.The report also stressed that British Crown Dependencies make a "significant contribution to the liquidity of the UK market". In the second quarter of 2009, they provided net funds to banks in the UK totalling $323 billion (£195 billion), of which $218 billion came from Jersey, $74 billion from Guernsey and $40 billion from the Isle of Man.

G20 tax havens blacklist

At the London G20 summit on 2 April 2009, G20 countries agreed to define a blacklist for tax havens, to be segmented according to a four-tier system, based on compliance with an "internationally agreed tax standard.” The list, drawn up by the OECD, was updated on 2 April 2009 in connection with the G20 meeting in London. Further changes were made to the list on 7 April 2009 to remove countries from the non-cooperative category. The four tiers are:

- Those that have substantially implemented the standard (includes countries such as Argentina, Australia, Brazil, Canada, China, Czech Republic, France, Germany, Greece, Guernsey, Hungary, Ireland, Italy, Japan, Jersey, Isle of Man, Mexico, the Netherlands, Poland, Portugal, Russia, Slovakia, South Africa, South Korea, Spain, Sweden, Turkey, United Arab Emirates, United Kingdom, and the United States)

- Tax havens that have committed to, but not yet fully implemented the standard (includes Andorra, the Bahamas, Cayman Islands, Gibraltar, Liechtenstein, and Monaco)

- Financial centres that have committed to, but not yet fully implemented, the standard (includes Chile, Costa Rica,[51] Malaysia,[51] the Philippines,[51] Singapore, Switzerland, Uruguay[52] and three EU countries – Austria, Belgium, and Luxembourg)

- Those that have not committed to the standard/ 'non-cooperative tax havens'. For the record is a complete list of non-cooperative tax havens as published by the OECD ( as per the printed edition of the Spanish newspaper El Pais dated April 4th, 2009.) In fact, there are three lists: the blacklist (countries that ignore foreign fiscal authorities) a grey list (countries that supposedly lack fiscal transparency but have committed to change) and a third list, neither grey nor black, of countries that are “non-co-operative financial centers.”

The Blacklist - Costa Rica, Philippines, Malaysia

The Grey List - Andorra, Anguilla, Antigua and Barbuda, Aruba, Bahamas, Bahrein, Belize, Bermuda, British Virgin Islands, Cayman Islands, Cook Islands, Cyprus, Dominica, Gibraltar, Grenada, Guernsey, Isle of Man, Jersey, Liberia, Liechtenstein, Malta, Marshall Islands, Mauritius, Monaco, Monserrat, Nauru, Netherlands Antilles, Niue, Panama, Saint Kitts and Nevis, Saint Lucia, Saint Vincent and Grenadines, Samoa, San Marino, Seychelles, Turks and Caicos Islands, US Virgin Islands, Vanuatu (Uruguay was oficially added to this list a few days later)

Non – Cooperative Financial Centres - Austria, Belgium, Brunei, Chile, Guatemala, Luxembourg, Singapore, Switzerland

Structured Finance

[Submitted by CA. Vibhuti Gupta,

Chartered Accountant,

New Delhi]

April 7, 2008

"Structured finance" is a broad term used to describe a sector of finance that was created to help transfer risk using complex legal and corporate entities.

Structure

Securitization

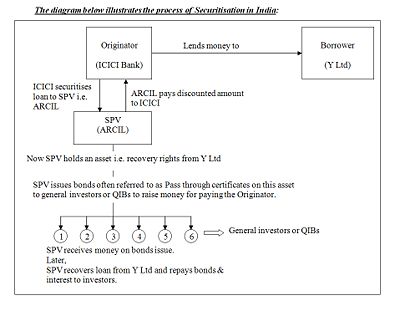

Securitization is a structured finance process, which involves pooling and repackaging of cash-flow producing financial assets into securities that are then sold to investors. The name "securitization" is derived from the fact that the forms of financial instruments used to obtain funds from the investors are securities.

All assets can be securitized so long as they are associated with cash flow. Hence, the securities, which are the outcome of securitization processes, are termed asset-backed securities (ABS). From this perspective, securitization could also be defined as a financial processes leading to an emission of ABS.

Securitization often utilizes a special purpose vehicle (SPV) (alternatively known as a special purpose entity [SPE] or special purpose company [SPC]) in order to reduce the risk of bankruptcy and thereby obtain lower interest rates from potential lenders. A credit derivative is also generally used to change the credit quality of the underlying portfolio so that it will be acceptable to the final investors.

A securitization transaction

Pooling and transfer

The originator initially owns the assets engaged in the deal. This is typically a company looking to raise capital, restructure debt or otherwise adjust its finances. For example, a company may provide 10 bn nominal value of leases, and it will receive a cash flow over the next five years from these. It cannot demand early repayment on the leases and so cannot get its money back early if required. If it could sell the rights to the cash flows from the leases to someone else, it could transform that income stream into a lump sum today (in effect, receiving today the present value of a future cash flow).

A suitably large portfolio of assets is "pooled" and sold to a special purpose vehicle (the issuer), a tax-exempt company or trust formed for the specific purpose of funding the assets. Once the assets are transferred to the issuer, there is normally no recourse to the originator. The issuer is "bankruptcy remote," meaning that if the originator goes into bankruptcy, the assets of the issuer will not be distributed to the creditors of the originator

Issuance

To be able to buy the assets from the originator, the issuer SPV issues tradable securities to fund the purchase. Investors purchase the securities, either through a private offering (targeting institutional investors) or on the open market. The performance of the securities is then directly linked to the performance of the assets. The securities can be issued with either a fixed interest rate or a floating rate. Fixed rate Asset Backing Securities set the "coupon" (rate) at the time of issuance, in the manner similar to corporate bonds. Floating rate securities may be backed by both amortizing and non - amortizing assets. In contrast to fixed rate securities, the rates on "floaters" will periodically adjust up or down according to a designated index. The floating rate usually reflects the movement in the index plus an additional fixed margin to cover the added risk

Credit enhancement and tranching

Securities generated in a securitization deal are "credit enhanced," meaning their credit quality is increased above that of the originator's unsecured debt or underlying asset pool. This increases the likelihood that the investors will receive cash flows to which they are entitled, and thus causes the securities to have a higher credit rating than the originator.

Individual securities are often split into tranches, or categorized into varying degrees of subordination. Each tranche has a different level of credit protection or risk exposure than another: there is generally a senior class of securities and one or more junior subordinated classes that function as protective layers for the senior class. The senior classes have first claim on the cash that the SPV receives, and the more junior classes only start receiving repayment after the more senior classes have repaid.. In the event that the underlying asset pool becomes insufficient to make payments on the securities (e.g. when loans default within a portfolio of loan claims), the loss is absorbed first by the subordinated tranches, and the upper-level tranches remain unaffected until the losses exceed the entire amount of the subordinated tranches. The senior securities are typically AAA rated, signifying a lower risk, while the lower-credit quality subordinated classes receive a lower credit rating, signifying a higher risk.

The most junior class (often called the equity class) is the most exposed to payment risk. In some cases, this is a special type of instrument which is retained by the originator as a potential profit flow. In some cases the equity class receives no coupon (either fixed or floating), but only the residual cash flow (if any) after all the other classes have been paid.

There may also be a special class which absorbs early repayments in the underlying assets. This is often the case where the underlying assets are mortgages which, in essence, are repaid every time the property is sold. Since any early repayment is passed on to this class, it means the other investors have a more predictable cash flow.

Servicing

A servicer collects payments and monitors the assets that are the crux of the structured financial deal. The servicer can often be the originator, because the servicer needs very similar expertise as the originator and would want to ensure that loan repayments are paid to the Special Purpose Vehicle.

Repayment structures

Most securitizations are amortized, meaning that the principal amount borrowed is paid back gradually over the specified term of the loan, rather than in one lump sum at the maturity of the loan

Structures are as follows :

A controlled amortization structure is a method of providing investors with a more predictable repayment schedule, even though the underlying assets may be non - amortizing. After a predetermined "revolving" period, during which only interest payments are made, these securitizations attempt to return principal to investors in a series of defined periodic payments, usually within a year. An early amortization event is the risk of the debt being retired early

A controlled amortization structure is a method of providing investors with a more predictable repayment schedule, even though the underlying assets may be non - amortizing. After a predetermined "revolving" period, during which only interest payments are made, these securitizations attempt to return principal to investors in a series of defined periodic payments, usually within a year. An early amortization event is the risk of the debt being retired early.

On the other hand, bullet or slug structures return the principal to investors in a single payment. The most common bullet structure is called the soft bullet, meaning that the final bullet payment is not guaranteed on the expected maturity date; however, the majority of these securitizations are paid on time. The second type of bullet structure is the hard bullet, which guarantees that the principal will be paid on the expected maturity date. Hard bullet structures are less common for two reasons: investors are comfortable with soft bullet structures, and they are reluctant to accept the lower yields of hard bullet securities in exchange for a guarantee.

Types

There are several main types of structured finance instruments.

-

Asset-backed securities (ABS) are bonds or notes based on pools of assets, or collateralized by the cash flows from a specified pool of underlying assets.

-

Mortgage-backed securities (MBS) are asset-backed securities whose cash flows are backed by the principal and interest payments of a set of mortgage loans.

-

Collateralized debt obligations (CDOs) consolidate a group of fixed income assets such as high-yield debt or asset-backed securities into a pool, which is then divided into various tranches.

-

Collateralized mortgage obligations (CMOs) are CDOs backed primarily by mortgages.

-

Collateralized bond obligations (CBOs) are CDOs backed primarily by corporate bonds.

-

Collateralized loan obligations (CLOs) are CDOs backed primarily by leveraged bank loans.

-

Credit derivatives are contracts to transfer the risk of the total return on a credit asset falling below an agreed level, without transfer of the underlying asset.

Stock or Share Split

[Submitted by CA. Vibhuti Gupta,

Chartered Accountant,

New Delhi]

May 5, 2010

Stock Split : It increases the number of equity shares in a public company. The price of shares is adjusted in such a way that the market capitalization of the company will remain the same after the split, so that dilution does not occur. Options and warrants are included. A stock split is a decision by the company's board of directors to increase the number of shares that are outstanding by issuing more shares to current shareholders

In other words : A stock split is a corporate action that increases the number of the corporation's outstanding shares by dividing each share, which in turn diminishes its price. The stock's market capitalization, however, remains the same, just like the value of the Rs 100 note does not change if it is exchanged for two Rs 50s. For example, with a 2-for-1 stock split, each stockholder receives an additional share for each share held, but the value of each share is reduced by half: two shares now equal the original value of one share before the split.

An example to explain stock split: Stock A is trading at Rs 400/stock and has 10 million shares issued, which gives it a market capitalization of Rs 4000 million (Rs 400 x 10 million shares). The company then decides to implement a 2-for-1 stock split. For each share shareholders currently own, they receive one share, deposited directly into their brokerage account. They now have two shares for each one previously held, but the price of the stock is split by 50%, from Rs 400 to Rs 200. Hence, the market capitalization stays the same - it has doubled the amount of stocks outstanding to 20 million while simultaneously reducing the stock price by 50% to Rs 200 for a capitalization of Rs 4000 million. The true value of the company hasn't changed one bit.

The most common stock splits are, 2-for-1, 3-for-2 and 3-for-1. An easy way to determine the new stock price is to divide the previous stock price by the split ratio. In the case of our example, divide Rs 400 by 2 and we get the new trading price of Rs 200. If a stock were to split 3-for-2, we'd do the same thing: 400/(3/2) = 400/1.5 = Rs 266.67.

A stock's price is also affected by a stock split. After a split, the stock price will be reduced since the number of shares outstanding has increased. In the example of a 2-for-1 split, the share price will be halved. Thus, although the number of outstanding shares and the stock price change, the market capitalization remains constant.

A stock split is usually done by companies that have seen their share price increase to levels that are either too high or are beyond the price levels of similar companies in their sector. The primary motive is to make shares seem more affordable to small investors even though the underlying value of the company has not changed.

A stock split can also result in a stock price increase following the decrease immediately after the split. Since many small investors think the stock is now more affordable and buy the stock, they end up boosting demand and drive up prices. Another reason for the price increase is that a stock split provides a signal to the market that the company's share price has been increasing and people assume this growth will continue in the future, and again, lift demand and prices.

Another version of a stock split is the reverse split. This procedure is typically used by companies with low share prices that would like to increase these prices to either gain more respectability in the market or to prevent the company from being delisted (many stock exchanges will delist stocks if they fall below a certain price per share). For example, in a reverse 5-for-1 split, 10 million outstanding shares at Rs 400 each would now become two million shares outstanding at Rs 2000 per share. In both cases, i.e., stock split & reverse stock split, the company is worth Rs 4000 million.

Different types of stock splits

Forward stock split: When any company will announce a forward stock split, the price of the stock will decrease; however, the number of shares will increase proportionately. For example, if you own 100 shares of XYZ Company that operates at Rs100/share, and it announces a two for one stock split, you will own a total of 200 shares at Rs 50.00 after the split. Although many stock splits are two for one, companies can split their stock in any number of ways, including three for one, three for two, and so forth. The stock market average returns for these new shares will reflect the ratio that was used in the split.

Advantages of Forward Stock Splits : The most important reason for a company to use this stock market strategy is to increase liquidity of the stock. Although there are investors buying certain companies stock at over Rs 100 per share, many more investors would be inclined to buy if there were five times more shares at Rs 50 per share. This tactic is employed by many companies when their stock sales come to a standstill because of the consistent increase in the prices of their stocks.

Reverse stock split: Reverse stock splits are less likely to be used by the companies as they show somewhat of a negative investment strategy attached to them. The reverse stock split is defined as the stock split under which a firm’s number of shares outstanding is reduced. If the price of a stock for a certain company drops too low, many mutual funds will not purchase them. Therefore, by having the low prices for their stocks, they run the risk of being delisted, or even being removed from the market indexes. In addition, the low stock prices of a company would create a psychological stigma as buyers and sellers view them as worthless. By doing a reverse stock split, companies can raise the stock price by lowering the number of outstanding shares; therefore, eliminating the problems caused by the low stock prices.

Advantages of Reverse Stock Split: There are three reasons why a company would want to go for a reverse stock split. First of all, the transaction costs to the shareholders would be less after the reverse stock split. Secondly, the liquidity and marketability of a company’s stock might be improved when its price is raised to the popular trading range. Finally, a stock selling at certain price below a certain level are not considered respectable which means that the investors underestimate these companies earnings, cash flow, growth, and stability. A reverse stock splits reduces the number of shares and increases the share price proportionately. For example, if you own 10,000 shares of a company and it declares a one for ten reverse split, you will own a total of 1,000 after the split. A reverse split has no affect on the value of what shareholders own.

Eligibility for stock split: Trading in the equity shares of the company should be in Compulsory Demat

Documents to be submitted prior to Corporate Action :

| Particulars | Timeline |

| Intimation of the Record Date / Book Closure for the Sub Division / Stock Split of the equity shares of the company with particulars. | At least 15 / 30 days in advance as applicable* |

| Certified true copy of the notice of Shareholders meeting for approval of the Sub Division / Stock Split of equity shares of the Company. | At the time of intimation of Record Date / Book Closure |

| Certified true copy of the shareholders resolution for the Sub Division / Stock Split of equity shares of the Company with detail proceedings. | At the time of intimation of Record Date / Book Closure |

| Details of issued and paid up equity share capital of the company pre & post Sub Division / Stock Split of equity shares of the Company. | At the time of intimation of Record Date / Book Closure |

| Undertaking from the company that all the beneficiaries will be credited with the split / sub divided shares in their respective demat accounts within one day from record date fixed for sub-division / stock split | At the time of intimation of Record Date / Book Closure |

| Intimation of activation of New ISIN Number along with Depositories’ confirmation of subdivided face value of the equity shares of the company to BSE | At least three days prior to Record Date / Book Closure. |

* Companies on whose stocks derivatives are available or whose stocks form part of an index on which derivatives are available at the time of fixing Book Closure/ Record Date, should give advance notice of at least thirty days while fixing Book Closure/ Record Date the company.

Documents to be submitted post Corporate Action

| Particulars | Timeline | Suggestive Format |

| Credit confirmation from the Depositories regarding all the beneficiaries having been credited with the split / sub divided shares in their respective demat accounts. | Within two days after the Record Date / Book Closure. | Copy of letter issued by Depositories |

| Specimen copies of Equity Shares Certificates | Within seven days after the Record Date / Book Closure. | N.A. |

| Certified true copies of amended Memorandum and Articles of Association. | Within seven days after the Record Date / Book Closure. | N.A. |

Suggestive Format

1. Intimation of Record Date / Book Closure

| Type of Securities | Date(s) of Record Date / Book Closures | Purpose | Benefit / Entitlement to the Shareholders |

2. Details of Issued and Paid up Capital

| Particulars |

Pre Corporate Action |

Post Corporate Action |

Number of Equity Shares

|

||

| Face & Paid-up Value of each Equity Share |

||

| Capital (in Rs.) |

||

| Distinctive Numbers |

3. Undertaking from the Companies (on Company’s Letterhead)

The Board of Directors of the Company has fixed a record date of DD/MM/YYYY for the purpose of sub-division / stock split of Rs. /- per share of the company into shares of Rs. /- each.

We hereby undertake that all the beneficiaries will be credited with the split / sub divided shares in their respective demat accounts within one day from record date fixed for sub-division / stock split i.e. DD/MM/YYYY.

Accounting aspects of Stock Split

Hence, only a memorandum notation in the accounting records indicates the decreased par value and increased number of shares.

- A Stock Split has NO effect on total:

- contributed capital

- retained earnings

- total stockholders' equity

- Reasons why no accounting treatment is prescribed for stock splits.

- Because the total par value of shares outstanding is not affected by a stock split (i.e., the number of shares times par value per share does not change)

- The share price would fully adjust to reflect the additional shares.

- It does not provide any dividend income to shareholders

Example for stock split: A stock split occurs when a Board of Directors authorizes a change in the par or stated value of its stock. This reduction in par value is made to lower the market price of the stock to make the stock more attractive to potential investors. When a company's stock splits, the change in the par value is offset by a corresponding change in the number of shares so the total par value remains the same. The total stockholders' equity is unaffected by the stock split and no entries are recorded. For example, if ABC Limited declared a 3-for-1 stock split , the company would issue three shares in place of every one share currently held. After the split occurs, the par value or stated value is divided by 3 (because it is a 3-for-1 stock split) to determine the new par or stated value, and the number of outstanding shares is multiplied by 3. After the stock split, the new par value is Rs100 (Rs 300 ÷ 3) and the number of outstanding shares is 150,000,000 (500,000 × 300). The total par value of the common stock remains at Rs 150,000,000 (1,500,000 shares × Rs 100 par value). The following chart illustrates the effects of stock dividends and stock splits on stockholders' equity :

| Particulars |

Before Stock Split |

After Stock Split |

|

Common Stock ( At Par ) |

150,000,000 |

150,000,00 |

| Additional Paid Up Capital | 60,000,000 | 60,000,000 |

| Retained Earnings | 23,250,000 | 23,250,000 |

| TOTAL SHAREHOLDER’S EQUITY | 233,250,000 | 233,250,000 |

| Shares Outstanding | 5,00,000 | 15,00,000 |

| Book Value Per Share | 466.50 | 155.50 |

STOCK SPLIT EFFECT ON STOCK'S PRICE

Impact on current stock holders : It means that the stock holder now has more shares in the company, but each share is priced less. Their overall value of stocks stays the same, though the price of stocks is generally affected by a stock split, and so there is a good chance the value of their stock will go up because of the stock split.

Effect on stock split on stock’s price: No & Yes –

No because : When the stock splits, the value of the stock as a whole stays the same. So, no the stock price is not effected. A stock holder still holds just as much value of stock as they did before. For example, while before a stock split an investor has 100 shares of stock at Rs 400/share, so they have Rs 40000 worth of stock. After the split they have 200 shares of stock at Rs 200/share, so they still have Rs 40000 worth of stock.

Yes because : As the price of a stock gets higher and higher, the stock becomes unaffordable for small investors, and thus they do not buy it, so the solution is to make the price per share less, but the value of each share less as well. Splitting the stock brings the share price down to a more "attractive" level, but the ownership in the company remains the same, there is just more stock to divide between. So, while the price changes, the value does not. However, the lower stock price may affect the way the stock is perceived and therefore entice new investors. So, as the stock becomes more affordable, more people buy it, and then the price goes up. Thus, the answer is yes because often as a result of splitting stocks, prices will rise.

The thing to remember with stock splits is that while the price and number of shares may change, the overall value of the stock stays the same.

The following are the most recent stock split announcements:

May 3, 2010:

General Mills, Inc. (NYSE:GIS) announced today that its board of directors approved a 2:1 stock split to be distributed beginning June 8, 2010.

Industrial Services of America, Inc. (Nasdaq:IDSA) announced today that its board of directors approved a 3:2 stock split to be payable on May 31, 2010.

April 29, 2010:

Baidu, Inc. (Nasdaq:BIDU) announced today that its board of directors approved a 10:1 stock split to be payable on May 11, 2010.

April 28, 2010:

TESSCO Technologies, Inc. (Nasdaq:TESS) announced today that its board of directors approved a 3:2 stock split to be distributed on May 26, 2010.

Green Mountain Coffee Roasters, Inc. (Nasdaq:GMCR) announced today that its board of directors approved a 3:1 stock split to be distributed on May 17, 2010.

April 12, 2010:

Edwards Lifesciences Corp. (NYSE:EW) announced today that its board of directors approved a 2:1 stock split to be distributed on May 27, 2010.

April 7, 2010:

BioReference Laboratories, Inc. (Nasdaq:BRLI) announced today that its board of directors approved a 2:1 stock split to be distributed on or about April 21, 2010.

Basic Terminologies used in International Taxation

[Submitted by Mr. Bhavik Bipin Mehta,

B.Com, C.S. Foundation, CA-PE-II, Articled Assistant

Mumbai, Maharashtra]

May 23, 2007

Economies are coming closer & closer due to globalization. Number of cross-border transactions has increased. Cross border transactions have led to a dynamic change in the system of taxation. New issues have aroused due to different styles of business arrangements. In the circumstances, it is important for an aspiring Chartered Accountant student to become verse with the basic understanding of different terminologies used in International Taxation.

The author is a second year articled assistant in an International Taxation firm and had the pleasure of attending the conference on International Taxation organized by Foundation for International taxation. He has made an attempt to explain the basic terminologies used in International Taxation parlance in a simplified manner (because of limitation of space, not much is elaborated on each of the terminologies):

Important sections in the Indian Income-tax Act:

| Sec. 2 (31) | - | Definition of a Person. |

| Sec. 2 (7) | - | Definition of an Assessee. |

| Sec. 6 | - | Conditions of Residence. |

| Sec. 5 | - | Scope of Total Income. |

| Sec. 9 | - | Income deemed to accrue or arise in India. |

| Sec. 4 | - | Charge of Income-tax. |

| Sec. 90 | - | Agreement with Foreign Countries. |

| Sec. 91 | - | Countries with which no agreement exists. |

| Sec. 92 | - | Computation of income from international transaction having regard to arms length price. |

| Sec. 92A | - | Meaning of Associated Enterprise. |

| Sec. 92 B | - | Meaning of International Transaction. |

| Sec. 92C | - | Computation of Arms Length Price. |

| Sec. 92D | - | Reference to Transfer Pricing Officer. |

| Sec. 93 | - | Avoidance of income-tax by transactions resulting in transfer of income to non-residents. |

| Secs. 115 A-F | - | Provisions relating to non-residents. |

Apart from these important sections, students must not forget to study the other relevant sections also.

1. Country of Residence:

Country where the person is tax resident under the relevant tax laws of any country is called the country of residence. Tax laws of all countries are different. At times, a taxpayer may be a resident of two countries. In such situations, he has to apply the tie-breaker test to become tax resident of only one country for the purposes of the double tax avoidance agreement (meaning of DTAA is explained in point no.11 & tie breaker tests can be seen in Article 4 - Resident of any DTAA ).

2. Country of Source:

Country where the person earns income or where the income accrues or arises is the country of source. In International Taxation parlance, it is the country where that person has done the value addition. Where the value addition is done is a big controversy in itself!

3. Country of Payment:

Country from which the person makes the payment is called the country of payment. Country of Source may not be the same as country of payment. Also, country of market/ consumption may or may not be the same as country of payment.

4. Country of Market/ Consumption:

Country where the actual consumption takes place is called the country of market/ consumption. Here also, country of source & country of payment may not be same as country of market/ consumption.

5. Tax Base:

There has to be a tax base for Government of different countries to charge tax. There can only 2 bases for levy of income-tax:

1. Residence.

2. Income.

For the levy of income-tax, Indian Government can tax the global income of Indian tax residents or the Indian accrued income of tax non-residents of India. Governments cannot tax foreign sourced income of non-residents. Prima facie they have no right to levy income-tax on foreign sourced income of non-residents.

There has to be a nexus between the country & its residents or the country & income sourced in that country. Unless & until, there is a nexus between any one of the two, Governments do not have a base/ jurisdiction for taxation.

6. Permanent Establishment (PE):

Sec. 92 F provides an inclusive definition of Permanent Establishment. The section says, "It includes fixed place of business through which the business of the enterprise is wholly or partly carried out."

Article 5 of OECD & UN model conventions also provide for an inclusive definition of the term permanent establishment i.e. "it includes a place of management, a branch, an office, a factory, a workshop and ..."

Attribution of profits to PE:

This is a major controversy in International Taxation i.e. How to attribute the profits to a permanent establishment?

The international consensus has been that the profits should be attributed to a PE on the basis of the "separate enterprise" concept, and the application of the arm's length principle. This is currently encapsulated in Article 7(1) and (2) of the OECD Model Tax Convention as follows:

"(1) The profits of an enterprise of a Contracting State shall be taxable only in that State unless the enterprise carries on business in the other Contracting State through a permanent establishment situated therein. If the enterprise carries on business as aforesaid, the profits of the enterprise may be taxed in the other State, but only so much of them as is attributable to that permanent establishment.

(2) Subject to the provisions of paragraph (3), where an enterprise of a Contracting State carries on business in the other Contracting State through a permanent establishment situated therein, there shall in each Contracting State be attributed to that permanent establishment the profits which it might be expected to make if it were a distinct and separate enterprise engaged in the same or similar activities under the same or similar conditions and dealing wholly independently with the enterprise of which it is a permanent establishment."

This means that PE should be hypothesized as separate unit. Accordingly, functions, risks, assets, capital employed, etc. should also be attributed to the Permanent Establishment for attributing profits to PE.

Governments cannot tax the business income of a non-resident in absence of a Permanent Establishment.

7. Business Connection:

Sec. 9 (i) explains business connection. It says it includes "any business activity carried out through a person who, acting on behalf of the non-resident-

(a) has and habitually exercises in India, an authority to conclude contracts on behalf of the non-resident, unless his activities are limited to the purchase of goods or merchandise for the non-resident ; or

(b) has no such authority, but habitually maintains in India a stock of goods or merchandise from which he regularly delivers goods or merchandise on behalf of the non-resident ; or

(c) habitually secures orders in India, mainly or wholly for the non-resident or for that non-resident and other non-residents controlling, controlled by, or subject to the same common control, as that non-resident :

Provided that such business connection shall not include any business activity carried out through a broker, general commission agent or any other agent having an independent status, if such broker, general commission agent or any other agent having an independent status is acting in the ordinary course of his business :

Provided further that where such broker, general commission agent or any other agent works mainly or wholly on behalf of a non-resident (hereafter in this proviso referred to as the principal non-resident) or on behalf of such non-resident and other non-residents which are controlled by the principal non-resident or have a controlling interest in the principal non-resident or are subject to the same common control as the principal non-resident, he shall not be deemed to be a broker, general commission agent or an agent of an independent status.

Explanation 3- Where a business is carried on in India through a person referred to in clause (a) or clause (b) or clause (c) of Explanation 2, only so much of income as is attributable to the operations carried out in India shall be deemed to accrue or arise in India. "

For better understanding of business connection & permanent establishment, kindly refer:

1. CIT v. R. D. Aggarwal & Co., 56 ITR 20 (1965) SC

2. Circular No. 1 of 2004 dated January 2, 2004.

3. Circular No. 23 of 1969 dated 23rd July, 1969.

4. Circular No. 5 of 2004 dated 28th September, 2004.

8. Associated Enterprises:

Sec. 92A subsection (1) provides for the meaning of Associates Enterprises. Sub-section (2) lists out the possible situations in which two enterprises will become associated enterprises.

Article 9 of OECD & UN model conventions also provide for the meaning & situations in which two entities will become associated enterprises. Identification of associated enterprises is very important for applicability of transfer pricing provisions.

9. Arm's Length Price - Transfer Pricing Methods:

Sec. 92 (1) says "any income arising from an international transaction (sec. 92B) i.e. a transaction between two or more associated enterprises, either or both of whom are non-residents shall be computed having regard to the arm's length price."

Sec. 92 C (1) read with rule 10 B provides for the methods to be used for computation of arm's length price. The Board has prescribed following 5 methods for calculation of arm's length price:

(a) comparable uncontrolled method,

(b) resale price method,

(c) cost plus method,

(d) profit split method,

(e) Transactional net margin method.

Transfer pricing refers to the price at which an associated enterprise of one country enters into a financial transaction with other associated enterprise of different country. The arm's length price is determined with the use of comparables. One has to calculate the arm's length price with regard to several factors like capital employed, risk undertaken, assets used by the associated enterprise, functions undertaken, etc.

Practically, it is very difficult to calculate the arm's length price. One has to use the most appropriate method out of the CBDT prescribed methods.

10. Double Tax Avoidance Agreements (DTAA):

Sec. 90 (1) gives power to the Government to enter into an agreement with the Government of any country outside India for granting relief in respect of double taxation, promotion of mutual economic relations, trade & investment, for the avoidance of double taxation, for exchange of information & for recovery of taxes.

Sec. 90 (2) states that provisions of Indian Income-tax or DTAA whichever is more beneficial to the assessee will apply i.e. in DTAA can even override the provisions of Indian Income Tax Act.

Tax treaties are signed for sharing of tax between the country of residence & country of source. Mr. Ankur Nishar, in his article on International Taxation in the May, 2007 newsletter has very rightly explained the concept of double taxation & DTAAs. So, I would not elaborate on this aspect.

11. Categorisation of Income:

Since different incomes will have different ways of determining the location of source; different categories have been listed. For e.g.: royalty, interest, dividend, fees for technical services, rental income, etc.

Under the DTA, it is necessary to determine the country of source of income. Since different incomes will have different ways of determining the country of source; different categories are useful to determine the source. The house property income is sourced in the country where the property is situated. The dividend income is sourced where the company distributing the dividend is resident. Salary income is taxable where services are performed. Thus for determining the location or the country of source, the categorisation is useful.

Under the domestic law, categorisation is useful for computation. Different categories of income may have different computation provisions.

12. Authority for Advance Ruling:

Sec. 245 N defines an advance ruling. Authority for Advance Ruling is a quasi judicial authority that helps the non-resident to know his taxability in India relating to a financial transaction in advance. This helps in avoiding controversies & litigation at a later stage i.e. after the financial transaction is undertaken. In the past, AAR has given several rulings. Unfortunately, with due respect, these rulings have put precedents that differ from the Tribunal, High Court or the Supreme Court decisions.

13. Tax Heavens:

A tax heaven is a country which does not charge tax to its residents or charges lower rates of tax. These countries sign the DTAAs with other countries in such a way, that there may not be any tax payable by the assessee in any country. Therefore, a lot many number of companies structure their investments so that they are outside the purview of any tax jurisdiction.

Countries like Isle of Man, Cayman Islands, Mauritius, Cyprus, Malta, Singapore, etc. are examples such tax heavens.

14. Treaty Abuse or Treaty Shopping:

Treaty shopping is nothing but shopping of the DTAA. Companies may take the benefit of the most beneficial DTAA. Generally, a treaty shopping arises when a resident of a State other than Contracting States of a tax treaty attempts to capitalize on benefits of the treaty by setting up a company with no economic substance or conducting a bogus transaction.

A good example of treaty shopping is that of Malaysia-Korea, India- Mauritius, etc.

Treaty shopping can occur in the following two ways:

1) A taxpayer of a country that has no treaty with the a particular country say India seeks the coverage of a favorable treaty,

or

2) A taxpayer of India treaty partner, prefers the treaty of another country.

15. Round Tripping:

Round tripping is the act of moving your funds outside the country & then channelising them back in the country to change the actual character of funds. Funds earned through illegal sources, etc. may be sent abroad & reinvested in the same country as legal funds. Companies use round tripping for changing the character of domestic funds into foreign funds or illegal funds into legal funds.

16. Hybrid Entities:

Hybrid entities are the different forms of entities. Say, for example, India gives the status of the firm as a tax resident. It taxes the firm on its income & the income of the firm is exempt in the hands of the partners.

In some countries, taxation is transparent i.e. it may not tax the income of the firm in the hands of the firm but it may tax the partners individually on income earned through the firm. There are also several other entities like US LLP, UK LLP, Dutch CV, German KG * Co., trust, partnership, co-operative societies, venture capital funds & collective investment vehicles, etc.; taxation of which may be separate in separate countries.

This may give rise to conflict in classification of cross border scenario. Hybrid entities may also give rise to complication in application of treaty provisions.

17. Tax Sparing:

Developing countries often attempt to attract foreign investors with incentives in the form of reduced rates of taxation or, in some cases, the exemption of certain types of income from tax. In order to preserve the resultant investment revenues to the developing country, the country of residence of the investor (that is, the developed country) "spares" the tax that it would normally impose on the low-taxed or untaxed income earned by its resident abroad by granting foreign tax credits equal to, or possibly greater than, the tax that would otherwise have been exigible in the developing country.

Tax sparing is intended to promote economic development among developing nations by ensuring that tax incentives offered to foreign investors by these countries were not eroded through the tax treatment of the income from the advantaged activities in the investor's country of residence.

18. Underlying Tax Credit:

Credit is available in residence country for taxes paid by subsidiaries of companies in foreign countries. The above can be explained with the help of following example:

Say, for e.g.: Company A in India has a wholly owned subsidiary in a foreign country. During the year, foreign subsidiary earns a profit of $ 1,000. Assuming tax rate in foreign country is 35 %, foreign subsidiary is liable to pay $ 350 in foreign country itself & shall remit the balance $ 650 in India. Foreign subsidiary will also have to pay a dividend distribution tax on this, say 15 % i.e. $ 97.5 on $ 650.

In India, Co. A will be taxed on its overseas subsidiary's profit. Since corporate taxes in India is, say we assume 30 %, then this translates to a tax of $ 300. But since a tax greater than this has been paid in the foreign country, no taxes are paid in India. In effect, Co. A has paid a tax of 44.75 % ($ 350 + $ 97.50) & tax credits of $ 147.5 is lost.

Pooling of foreign tax credits:

If however India would have permitted pooling of foreign tax credit, then even $ 147.5 would have been available as credit.

Many international treaties signed provide for underlying & pooling tax credits.

19. Non-Discrimination Clause:

Article 24 of OECD & UN Model Convention provide for subjecting the residents of one country to taxation & requirement connected therewith in other country similar to that of the residents of that other country i.e. the taxation & connected requirements should not be more burdensome than subjected to residents of that other country.

20. Limitation of Benefits:

Many persons were using the provisions of treaties to their own benefits. Some persons have even misused the treaty provisions by forming conduit, shelf, offshore companies or SPVs i.e. Special Purpose Vehicles.

Limitations on benefits provisions generally prohibit third country residents from misusing treaty benefits. For example, a foreign corporation may not be entitled to a reduced rate of withholding unless a minimum percentage of its owners are citizens or residents of the treaty country.

Article 23 of the UK - USA treaty provides for limitation of benefits clause.

Recently Indo- Singapore treaty was amended to insert the limited version of limitation of benefits clause. Indian tax authorities are also trying to re-negotiate tax treaties with UAE, Cyprus, Mauritius to insert this limitation of benefits clause.

21. Mutual Agreement Procedure (MAP):

Article 25 of the OECD & UN Model Convention state that where a person considers that the actions of his domestic country or the other country shall result in taxation not in accordance with the treaty provisions, irrespective of the remedies provided by the domestic law of those states, he can present his case to the competent authority in the country of his residence.

The competent authority of residence country shall verify the arguments stated whether the arguments are justified & if the case of unable to arrive at a satisfactory solution as regards elimination of the double taxation or interpretation of tax treaty, competent authorities of both the countries shall resolve the difficulties by mutual agreement.

22 Advanced Pricing Arrangements (APA):

An APA is an arrangement between a taxpayer and the tax authority wherein the method of determining the transfer pricing for inter-company transactions are set out in advance. Such programmes are designed to resolve actual or potential transfer pricing disputes in a cooperative manner. The tax payer must submit a formal APA application, tax authorities shall review & evaluate the proposal & then negotiate and execute the APA.

An APA:

- provides your business with certainty on an appropriate transfer pricing methodology, enhancing the predictability of tax treatment of your international dealings,

- substantially reduces or eliminates the possibility of double taxation in the future,

- provides a possible solution to situations where there is no realistic alternative way of both avoiding double taxation and ensuring that all profits are correctly attributed and taxed,

- limits the prospect of a potentially costly and time-consuming examination of major transfer pricing issues that would arise in the event of a transfer pricing audit, and lessens the possibility of protracted and expensive litigation,

- places your business in a better position to predict costs and expenses, including tax liabilities,

- reduces the record keeping burden on your business as you know in advance what records you are required to keep to substantiate the agreed methodology, and

- reduces your business costs, as no fee is charged for the APA.

23. Withholding tax at source:

Withholding tax is additional tax imposed by the country of source when various types of remuneration (dividends, interest, royalties etc.) are paid in favour of non-residents of that country. The principle of a withholding tax is that it is withheld (retained) by the payer and given directly to the taxation authorities. The payee is given only the balance after the withholding tax amount. The primary motivation is to reduce tax evasion or failure to pay.

24. Force of Attraction rule:

Normally, business profits are taxed in the country of residence except when the entity functions or performs business in the other country with the help of a dependent agent or a permanent establishment. In such cases, income attributable to the permanent establishment is taxed in the country of source. The Contracting States will attribute to a permanent establishment the profits that it would have earned had it been an independent enterprise engaged in the same or similar activities under the same or similar circumstances.

As the name suggests, the force of attraction approach focuses on the actual economic connection between a particular item of income and the permanent establishment. Under the "force of attraction" approach, all domestic sourced income is attributed to the permanent establishment, irrespective of whether the relevant item of income is in fact economically connected with the activity of such a permanent establishment.

25. Controlled Foreign Corporations (CFC) rules:

Income from a foreign source is taxed usually after it is accrued or received as income in the country of residence of the taxpayer. The use of intermediary entities in a tax-free or low-tax jurisdiction enables a tax resident to defer (or avoid) the domestic tax on the income until it is repatriated to the residence state. This tax deferral could lead to an unjustifiable loss of domestic tax revenue.

A CFC is a legal entity that exists in one jurisdiction but is owned or controlled primarily by taxpayers of a different jurisdiction. CFC laws can be introduced to stop tax evasion through the use of offshore companies in low-tax or no-tax jurisdictions such as tax havens. It is rarely illegal to have a financial or controlling interest in a foreign legal entity; however, many governments require taxpayers to declare their interests and pay taxes on them, and CFC laws (combined with a no-tax jurisdiction or a double taxation agreement) sometimes mean that a company is only taxed in one jurisdiction.

The CFC rules are designed to stop companies avoiding tax in residence country by diverting income to subsidiaries situated in low tax regimes.

Students are requested to read articles, books written by Professor Klaus Vogel, OECD Model Tax Convention & Commentary, UN MTC & Commentary, League of Nations report, Vienna Convention reports, IFA reports, etc. Students are also requested to read the recent AAR & Supreme Court decisions for thorough understanding of International Taxation.

Some Tips for Examinees of CA and other Professional Courses

[Submitted by CA. Dev Kumar Kothari,

B.Com, Grad.CWA, ACS, FCA,

Kolkata]

April 14, 2007

"The result of examination would depend on what and how you write during examination hours (usually three hours) and how the examiner consider your answers in 10-15 minutes when he checks your answer book and evaluate your answers".

Stop reading at least three hours before examination- have confidence in memory recall. Memory recall will be better if your mind is relaxed and ready to work vigorously, your fingers will be faster to write during 180 minutes - and that will give you better result.

Do some exercises, yoga, meditation and light massage on entire body and slight vigorous massage on your head, forehead and fingers - 20 minutes

Have a good bath for at least fifteen minutes, sprinkle water on entire body, and specially on your eyes and head sit in bath tub singer. - 20 minutes.

Sit in your pooja room have a ghee /oil lamp lightened and concentrate on the light of the lamp for at least ten minutes in two or more exercises, before you leave your home for examination. This will improve your concentration. Have faith and confidence in your god- this will improves your self-confidence. Students not at home but at some other place can even use candle light or nigh lamp for this purpose.- 15 minutes.

Have light food that is easily digestible and provide you strength and stamina for four -five hours. Relax in lying condition for 15-20 minutes after taking food.

Be ready and leave for examination centre. Sufficient time should be kept in view of distance, mode of transportation, usual time and time for contingency to ensure that you reach the examination centre at least 30 minutes before the examination starts.

Drink water, tea / coffee , visit urinal and then sit on your seat at least fifteen minutes before time for commencement of examination. Have relaxed mood and try to have self-confidence.

On the examination answer book write properly relevant information about roll no, code no. subject name and code, part of paper etc. On each page write PTO. During this time you can, (with generally implied permission) also write abbreviations which you are likely to use / intend to use while answering questions considering the subject. For example:

C.G. means the Central Government.

S.G.= the State Government.

Authority = the appropriate / concerned authority.

Act = The Act means the relevant enactment /Act in the context of Question..

Rules = the Rules means the relevant Rules in the context of question.

A.O. = the assessing officer,

ROC = Registrar of companies.

RD = Regional director.

MOA= Memorandum of Association.

SC= The Supreme Court of India, HC = High Court

Dr = debit , Cr= Credit, S. = section, R.= Rule, P/ l = Profit and loss account, B.S.+ Balance sheet ...

More abbreviations which you are required to use while answering questions can be written while answering questions.

This can be arranged in tabular form with two or more columns.

The answer sheets can be folded so as to create four or eight columns for improvement in presentation and reducing time for putting lines with scale. In case of theory papers the answer book can be folded on right side to provide margin space.

Relax - close eyes have deep breaths remember Maa Saraswati.

On receipt of question paper:

Read instructions about compulsory question, total questions in paper and questions to be answered, questions with options etc.

You consider that for each mark you have 1.5 minutes for writing answers requiring 150 minutes and balance 30 minutes are for reading question, understanding words used in the question, planning answer and review etc.

Careful reading of question is very important, each word in question is important and has its significance.

Do not read entire question paper - it may be sheer wastage of time because most of the questions have to be attempted.

Do not start with compulsory question and questions carrying more marks. These are generally tough, intricate and very lengthy and some times confusing.

At initial time stamina is generally weak, attempting compulsory question or question carrying higher marks, generally dampens stamina. Therefore, attempt some smaller questions during first 30-45 minutes or one hour. By attempting to smaller questions first, you may be able to answer questions carrying 40-50 marks within first hour. This will give you more confidence , stamina and tempo will be improved to face more tough and lengthy questions. Now time available per minute for other questions will be more. For example ,suppose within first eighty minutes you have attempted questions carrying 60 marks ( saving 10 minutes from budgeted 90 minutes), then you have 100 minutes at your disposal for answering questions carrying 40 marks that is 2.5 minutes for each mark.

After each answer keep some space blank so that at the time of review you can add further points if they come in mind.

During second hour, (or after 80-85 minutes only) start answering questions, which are compulsory, carry higher marks and are lengthy.

During last 5-10 minutes review answers check that question nos. and sub question nos. are written correctly, properly tag extra sheets used, put necessary information about code no. etc. mark each page of additional sheet also with PTO. So that the examiner is requested to see all pages, even if any page is left blank in hurry or inadvertently.

In between drink some water, and tea / coffee or cold drink as suits you (you may carry in flask). Some times application of vicks or other pain balm may be useful to stimulate mind and to change mood.. So these items may be kept with you. These depends on personal habits.

Take intermittently deep breaths for 30-40 seconds each time (which one can easily do while reading question paper as well as writing) some times at intervals of 30-40 minutes means 6-7 times during examination hours. This will keep you fresh and more attentive.

At last while tagging the answer sheets, and handing over the answer book pray the god that the examiner should be in good mood and have some sort of synchronized thinking with yours, while checking your answer book.

"RELATIVE" - A brief study as dealt by the Companies Act, 1956

[Submitted by Pavan K.,

Bellary, Karnataka]

November 30, 2006

- Sec 2(41) --> "Relative" means with reference to any person, any one who is related to such person in any of the ways specified U/s 6 and NO others.

- Sec 6 -->

a) This is substituted by sec.4, Act 65, 1960.

b) "A Person shall be deemed to be a relative of another if and only if:

i) they are members of a Hindu Undivided Family,

ii) they are husband & wife,

iii) one is related to the other in the manner indicated in schedule - I A"

c) Schedule - I A was inserted by Act 65, 1960 with 49 types of relationships vide List of Relatives to Companies Act, 1956.

d) However, courtesy Companies Amendment Act, 1965, w.e.f 15-10-1965 27 types of relationships were omitted (i.e. from Nos. 23 - 49)

e) Thus, the law as stands today 22 types of relationships subsists (For details please refer Schedule - I A of the Companies Act, 1956 as amended up-to-date)

f) They are succinctly grouped as under:

i) Father - Mother 2 ii) Parents of Father & Mother

(I.e. Paternal as well as Maternal grand parents)4 iii) Son - Son's Wife 2 iv) Children with spouse of (iii) above 4 v) Daughter - Daughter's husband 2 vi) Children with spouse of (v) above 4 vii) Brother - Brother's wife 2 viii) Sister - Sister's husband 2 22

Notes:

1) Mother includes Step-Mother

2) Son includes Step-Son

3) Brother includes Step-Brother

4) Daughter includes Step-Daughter

5) N.B: (B's) spouse's parents i.e. Father-in-law & Mother-in-law are NOT relatives as per schedule - I A of the Companies Act, 1956.

- It may not be out of place to note here that section 6 begins with the phrase "Meaning of Relatives".

- According to Interpretation of Statutes - A particular expression is often defined by the legislature by using the word "MEANS" or the word "INCLUDES" or "MEANS and INCLUDES". However, in the context of section 6, the word used is "Meaning", which indicates that the definition is hard and fast definition, and no other meaning can be assigned to the expression than is put down in the definition.

- Thus, when the word means is used in the definition is prima facie restrictive & exhaustive. Whereas, when word "Includes" is used, the definition is prima facie extensive.

- Please note: Definition given in a statute is not always exhaustive unless it is expressly made clear in the statute itself. (Kalpanath Rai Vs. State (1997) 8 SCC 732.

- According to Interpretation of Statutes - A particular expression is often defined by the legislature by using the word "MEANS" or the word "INCLUDES" or "MEANS and INCLUDES". However, in the context of section 6, the word used is "Meaning", which indicates that the definition is hard and fast definition, and no other meaning can be assigned to the expression than is put down in the definition.

- Departmental Clarification: - Reverse Relationships not specified: Sub-section (c) of section 6 of the Companies Act, 1956 does not cover any reciprocal relationships in the reverse direction in the case of any of the relatives enumerated in the schedule except those expressly included in the schedule itself.

- Departmental Clarification: -

- Relatives of a deceased spouse (Deemed to be relatives U/s 6)

- Relationship by half blood

Examples: a) Step Mother

b) Step Son / Daughter

c) Step Brother

- Person given away adoption, ceases to be a relative

- Relatives of a deceased spouse (Deemed to be relatives U/s 6)

- The definition U/s 6 does not cover an illegitimate child

(Lakshmikutty Vs. Mohandas AIR 1990 Ker 78,81

- Provisions under Companies Act, 1956 where definition of relative is relevant:

a) Sec 3(1)(iii)(d) --> Prohibition w.r.t. A private company from making any invitation or accepting or deposits from persons other than its members, directors or their relatives.

b) 314 --> Director, etc. not to hold office or place of profit.

c) 294AA --> Power of Central Government to prohibit the appointment of sole selling agent in certain cases.

d) 295 --> Loans to Directors, etc.

e) 297 --> Board's sanction to be required for certain contracts in which particular directors are interested.

- The expression "Members of a Hindu Undivided Family" is a wider term than "Coparceners" and includes all female members, including the wives of coparceners.

Departmental Clarification F.No. 8/16(1)/62 - PR

Distribution of Overhead in Small Scale Industry

[Submitted by Mr. Anshul Rastogi,

CA(Final) Student]

September 27, 2006

Overhead is expenses incurred for carrying out the production process and sale of finished goods. On the other hand overhead is an indirect cost i.e. cost does not directly attributable to any department. All overhead expenses must have identification for department or product except in cases where this is not possible. Various approach are used for allocate and apportionate overhead to the department.There is little difference between allocation and apportionment of overhead. The dictionary meaning of allocation is 'To Place' and dictionary meaning of apportionment is 'To Share'. According to ICMA Terminology "The allotment of whole item of cost to cost centers or cost unit is know as allocation." The term apportionment is defined as allotment to two or more cost center or cost unit of a proportion of common item of cost on estimated basis of benefit received. The service department expenses have to be further apportioning to the department on some equitable basis depending up on the nature and extent of service rendered. The process of allocation or apportionment of overhead to the department is called as departmentalization of overhead. These department or product is called as cost center to which all cost is charged through allocation and apportionment.

In perspective of India two approach is famous to allocate and apportionate overhead viz. traditional approach and modern approach (Activity Based Costing).

I. Traditional Approach:

This approach is very famous approach to allocate and apportionate overhead up to 1950's in India. In this approach indirect cost that directly identifiable to the department is allocate and expense incurred for various department jointly have to be apportionate over each department on proportionate basis. Proportion can be differing from expense to expense. For examples:

| Expense | Basis for apportionment |

| Rent | Area occupied |

| Lighting | No. of switches |

| Salary | Time devoted |

| Power | No. of machine x Horse power of machine |

It is necessary to take best suitable proportion to apportionate overhead for ascertain cost. In this approach every customer pay equal amount for product irrespective of facility enjoyed.

II. Modern Approach (Activity Based Costing):

With the rapid advancement in industrialization with all its complexities a new approach is introduced to allocate and apportionate overhead named Activity Based Costing. Under this approach all indirect cost are traced to departments on the basis of activity carried for production. The great advantage of this approach is that customer who enjoyed more facility pay more and who enjoyed less facility pay fewer amounts.

In both approach profit of the company is same department-wise profit can be changed. Activity Based Costing (ABC Technique) is world wide acceptable costing technique. Big manufacturing concern can adopt ABC Technique because it evaluates correct performance of each department.

In the perspective of India small-scale industry can not adopt ABC Technique because it is very technical system and require a person who has technical knowledge of ABC Technique. This system is very expensive system because it require more cost records and cost books. Small-scale industry can adopt a new technique named Hybrid Technique easily. Under this approach some indirect expense who play relevant role in ascertainment of cost apportionate on the basis of activities and other expense apportionate on proportionate basis depending up on the nature of expense. Hybrid technique is less expensive, less technical and requires less costing records in compare to Activity Based Costing.

Illustration:

A small-scale industry manufactures three products A, B and C. Product A is manufacture in department X, product B is manufacture in department Y and product C is manufacture in department Z. there is two service department viz. canteen and maintenance. Information relating to direct cost to these departments is given below:

|

Departments |

|||||

| Particular | X | Y | Z | Canteen | Maintenance |

| Direct Material | 50000 | 20000 | 10000 | 25000 | 10000 |

| Direct Labor | 20000 | 10000 | 5000 | 15000 | 40000 |

| Other information: | |||||

| No. of employees | 100 | 50 | 20 | 10 | 5 |

| Area occupied (in square feet) | 1000 | 500 | 200 | 100 | 50 |